Income Tax Act, 1961 - Sections 92C(3), 92(1), 9(1)(vi) and 9(1)(vii) - The case pertains to a foreign entity incorporated in the Netherlands providing various services to its Indian associated enterprises (AEs), including LNG storage services, manpower services, software licensing, and technical advisory. The Assessing Officer (AO) and Transfer Pricing Officer (TPO) made upward adjustments to the value of international transactions under transfer pricing provisions. The AO also treated certain receipts as "royalty" and "fees for technical services" (FTS) under sections 9(1)(vi) and 9(1)(vii) of the Act. The objections raised by the taxpayer before the Dispute Resolution Panel (DRP) were rejected. The entity challenged the adjustments before the Tribunal, arguing that they violated DTAA provisions and transfer pricing principles - Whether the transfer pricing adjustments for services provided to the Indian AEs were justified under the arm's length price (ALP) mechanism - Whether receipts from software licensing and other services could be classified as "royalty" or "fees for technical services" under section 9(1)(vi), 9(1)(vii) of the Act, and the India-Netherlands DTAA - Whether the adjustments made were in violation of the principle of base erosion or the "mirror ALP" concept - HELD - The Tribunal rejected the argument that ALP adjustments violated the base erosion principle. Referring to the Special Bench decision in Instrumentarium Corporation Ltd., it held that ALP adjustments made to the income of a foreign entity do not warrant a corresponding deduction in the hands of the Indian AE unless expressly provided by law. It observed that base erosion could not be invoked as the adjustments do not lower the Indian tax base - Regarding software payments treated as royalty, the Tribunal applied the Supreme Court's ruling in Engineering Analysis Centre of Excellence Pvt. Ltd. and held that payments for off-the-shelf software do not qualify as "royalty" since they do not transfer any copyright to the user - For FTS, the Tribunal noted that the relevant DTAA contains a "make available" clause, meaning that services must enable the recipient to apply the technical knowledge independently in the future. It found that the services provided did not meet this requirement, and therefore, such payments could not be taxed as FTS under the DTAA - The "mirror ALP" argument was also rejected. The Tribunal held that ALP adjustments in one entity do not automatically necessitate corresponding adjustments in related entities unless explicitly provided for in the Act - The Tribunal partly allowed the appeal. It directed the TPO to conduct a fresh comparability analysis for certain transactions and deleted the additions made under the "royalty" and "FTS" classifications, citing DTAA provisions and the principles laid down by the Supreme Court

2025-VIL-01-ITAT-AHM

IN THE INCOME TAX APPELLATE TRIBUNAL

“D” BENCH AHMEDABAD

ITA No. 2390/Ahd/2018

CO NO.20/Ahd/2022

Assessment Year: 2014-15

1783/Ahd/2019

Assessment Year: 2015-16

Date of Hearing: 05.09.2024 & 06.12.2024

Date of Pronouncement: 18.12.2024

SHELL GLOBAL SOLUTIONS INTERNATIONAL B.V.

Vs

ACIT

Assessee by: Shri S.N. Soparkar, Sr. Advocate, and Shri Parin Shah, AR

Revenue by: Dr. Darsi Suman Ratnam, CIT-DR

BEFORE

SMT.ANNAPURNA GUPTA, ACCOUNTANT MEMBER

SHRI T.R. SENTHIL KUMAR, JUDICIAL MEMBER

ORDER

PER ANNAPURNA GUPTA, ACCOUNTANT MEMBER

The above appeals relate to the same assessee and are filed against orders of the Asstt. Commissioner of Income-tax (International Taxation), Ahmedabad dated 3.10.2018 and 19.9.2019 for the assessment years 2014-15 and 2015-16 respectively passed under section 143(3) read with section 144C of the Income Tax Act, 1961 ("the Act" for short). The Revenue has filed cross-objection in the assessee’s appeal for Asst.Year 2014-15 above.

2. It was common ground that the issues raised in both the set of appeals were identical. Therefore, both the appeals & CO were heard together and are being disposed of by this common consolidated order.

3. At the outset itself, it was stated by the Ld.Counsel for the assessee that the issues arising in the assessee’s appeal were all legacy issues arising from year to year right from the Asst. Year 2007- 08 onwards upto the immediately preceding assessment year i.e. Asst. Year 2013-14 and all adjudicated by the ITAT. Therefore, it was stated that all the issues were covered by the decision of the ITAT in the preceding years in the case of the assessee.

It was, however, stated that with respect to the issues raised regarding transfer pricing adjustment made to the international transactions entered into by the assessee there were some distinguishing facts/proposition of law which needed to be brought to the notice of the Bench/argued before the Bench, and therefore, with respect of the said ground, exhaustive arguments needed to be made for the assessee. With respect to the other remaining grounds, it was stated that no distinguishing facts or proposition of law needed to be pointed out.

Having stated so, the appeals were proceeded to be argued with.

4. Both the parties were heard. Since, admittedly, the issues raised in both the appeals of the assessee, pertaining to the Asst.Year 2014-15 and 2015-16, are identical we shall deal with the grounds raised by the assessee in Asst. Year 2014-15 and our decision rendered therein will apply pari passu to the appeal of the assessee for Asst. Year 2015-16.

ITA No.2390/Ahd/2018 – assessee’s appeal for Asst. Year 2014-15

5. Ground No.1 raised by the assessee reads as under:

“1. Transfer Pricing Adjustment of INR 220,39,59,249

1.1. The learned AO / TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO / TPO on the fact and in law in applying the transfer pricing ('TP') provisions and making a TP adjustment of Rs.215,34,57,741 to the value of international transactions entered into by the Appellant with Hazira LNG Private Limited ('HLPL') in respect of rendering services in relation to operation of LNG storage and regasification.

1.2. The learned AO / TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO / TPO on the facts and in law in applying the TP provisions and making a TP adjustment of Rs.5,05,01,507 to the value of international transactions entered into by the Appellant with Shell India Markets Private Limited ('SIMPL') in respect of rendering of manpower services.

The Appellant prays that the TP provisions are not intended to apply where the adoption of the arms-length price would result in a decrease in overall tax incidence in India.

1.3. The learned AO / TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO / TPO on the facts and in law in misinterpreting directions of the learned DRP in earlier years, wherein learned DRP has accepted the legal position that the TP provisions cannot be applied where the adoption of the arm's length price would result in a decrease in overall tax incidence in India, however, TP adjustment was upheld on account of the losses incurred by HLPL and SIMPL in the respective years, without appreciating the facts that:

• HLPL has started making profits from AY 2012-13 and onwards; and

• SIMPL has started paying tax on the assessed income from AY 2012-13 and onwards.

1.4. Without prejudice to the above, on the facts and in the circumstances of the case and in law, learned AO / TPO has erred and learned DRP has further erred in confirming the TP adjustment with respect to the income from services mentioned above, from HLPL and SIMPL by not allowing the benefit of provisions of Article 9(1) of India -Netherlands Tax Treaty ('DTAA') being more beneficial to the Appellant than the provisions of the Income-tax Act, 1961 ('the Act') and by virtue of section 90(2) of the Act.

1.5. Without prejudice to the above, on the facts and in the circumstances of the case and in law, learned AO / TPO has erred and learned DRP has further erred in rejecting the approach of the Appellant of comparing the fixed and optional services provided to HLPL with respective fixed and optional services provided to comparable company.

1.6. Without prejudice to the above, the Appellant humbly submits that in case, if the contention of the Appellant on the non-taxability of INR 8,74,34,868 (received from HLPL) as fees for technical services under Article 12 of DTAA (as per Ground No. 4 below) is accepted, then the corresponding transfer pricing adjustment in relation to the services rendered to HLPL should also be reduced to that extent.”

6. The above ground, it was contended, pertained to the Transfer Pricing (TP) adjustment made to the international transactions undertaken by the assessee with its Associate Enterprise (AE).

7. Giving a brief background of the case, it was pointed out that the assessee-company, M/s. Shell Global Solutions International BV was incorporated in 1998 and engaged in coordinating operation of a number of Royal Dutch Shell entities world-wide. The assessee company provided research and technical services to a range of petroleum related industry segments including additive process industries; automotive and supply, exploration and production, chemical, gas and liquefied natural gas (LNG) processing, motorsports, refining, marketing and supply and distribution. Its services included chemical analysis, crude oil evaluation, engineering, energy optimization, gas-to-liquids conversion, re-gasification, hydro cracking, inspection, thermo-analysis and water treatment.

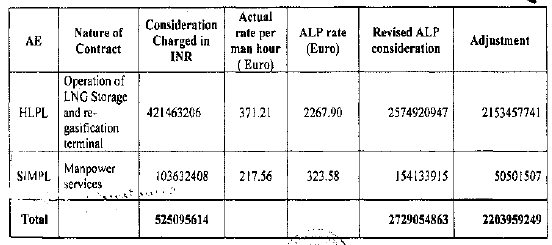

8. The assessee-company, during the impugned year, had provided services of operations of LNG storage and re-gassification terminal to its AE, i.e. Hazira LNG P. Ltd. (“HLPL”) and received an amount of Rs.421,463,206/- for the said services. Similarly, the assessee company provided manpower services to another AE, Shell India Markets P.Ltd. (“SIMPL”) during the impugned year and charged/received an amount of Rs.103,632,408/- for the said services. These international transactions were referred by the AO to the TPO for TP analysis who noted that the average hourly rate charged by the assessee from its AE, “HLPL” ,at the rate 217.56 EURO per man hour for the operation of LNG storage and re-gasification terminal ,was far less as compared to the similar services provided to a third party i.e. Brunei LNG to which a higher rate of 2,267.90 EURO per man hour had been charged. Taking this third party rate as an internal CUP, the TPO applied the same for benchmarking the international transaction of provision of services related to the operation of LNG storage and re-gasification terminal to its AE HLPL, resulting in an upward adjustment of Rs.215,34,57,741/- to the said international transaction.

9. Similarly, with regard to the provision of manpower services to other AE, “SIMPL” the TPO noted that while the assessee had charged a rate of 217.56 per man hour, however with regard to a third party the rate charged was much higher of 323.58 EURO. Taking this third party rate of 323.58 EURO per man hour as an internal CUP for benchmarking of international transaction of provision of manpower services, the TPO proposed an upward adjustment of Rs.5,05,01,507 to the international transaction of provision of man power services to its AE, SIMPL.

In the result, the TPO proposed a total upward adjustment of Rs.220,39,59,249/- to the international transaction entered by the assessee with its AE, HLPL and SIMPL. The upward adjustment proposed by the TPO are tabulated in his order as under:

10. The assessee objected to the proposed upward adjustment to the DRP, who noted that this issue was under consideration before the DRP consistently in earlier years, i.e. Asst. Year 2007-08 to 2024-15 and the DRP had consistently rejected the objection of the assessee in the said years. The DRP also noted that, the assessee had carried the matter in appeal before the ITAT in Asst. Year 2007-08 and 2010-11 and all the contentions of the assessee had been rejected by the ITAT. Following the decision of the ITAT in the assessee’s own case, and the consistent view of the DRP in the case of the assessee in the preceding year, the DRP rejected the objection of the assessee.

Aggrieved, the assessee has come up in appeal before the Tribunal.

11. The ld. counsel for the assessee contended that one of the arguments which was raised in the preceding year, and which did not find favour both with the DRP and the ITAT was the base erosion principle. The ld. counsel for the assessee pointed out that it had argued that by virtue of upward adjustment made to the ALP of the international transaction in the hands of the assessee, a corresponding adjustment to the expenses incurred in the hands of the Indian AE was warranted and as a consequence, while, the assessee would be liable to pay tax at the rate of 10% on the TP adjustment made, the Indian AE would be liable to a refund since it would be subjected to tax at the rate of 33% and the corresponding expense increase would result in a refund of tax to it. The assessee it was pointed out had argued that, in fact, as a consequence there was base erosion on account of ALP adjustment made in the hands of the assessee, and therefore, in terms of provision of section 92C(3) of the Act the TP provisions were not attracted.

12. The ld. counsel for the assessee pointed out that in the preceding years these arguments of the assessee had been rejected. The reason being that when the issue was pending before the ITAT in the case of the assessee for Asst.Year 2007-08 to 2010-11, this particular issue was taken up by the Special Bench of the ITAT for adjudication, and the assessee was an intervener in the said case. The Special Bench of the ITAT in the case of Instrumentarium Corporation Ltd. Vs. CIT, ITA No.1548 and 1549/Kol/2009 (SB) thereafter dealt with the issue at hand in the case of the assessee also and ruled against the assessee rejecting the assessee’s arguments of there being base erosion on account of ALP determination in the hands of the assessee. Applying the said decision the Special Bench the ITAT, this argument of the assessee was rejected in the order passed by the ITAT for all Asst.Year right from A.Y 2007-08 to the immediately preceding assessment year i.e. 2013-14.

13. The ld. counsel for the assessee contended that there was a distinguishing fact in all these years with the impugned year. He contended that the assessee’s argument of base erosion was rejected in the preceding years noting that the AEs were incurring loss, and therefore, it was held that on account of ALP adjustment made in the hands of the assessee there was no base erosion. The ld. counsel for the assessee contended that it was in these facts and circumstances that the base erosion arguments of the assessee had been rejected both by the Special Bench of the ITAT in the case of the assessee. He stated that the facts in the present case are, however, different and the assessee has made profits, and also paid taxes in the impugned year. In support of his contentions that the base erosion arguments need to be accepted, reliance was placed on the decision of the ITAT Pune Bench in the case of Cummins Inc. Vs. ADIT (2016) 73 taxmann.com 207 (Pune). The assessee also relied on the decision of Hon’ble Apex Court in the case of CIT Vs. Glaxo Smithkline Asia P.Ltd., (2010) 195 Taxman 35 (SC) for the proposition that there ought to be no ALP adjustment if it is a revenue neutral exercise.

14. Having heard contentions of the ld. counsel for the assessee, and having gone through the orders of the Special Bench in the case of Instrumentarium (supra), as also decisions in the case of the assessee in the preceding year, we do not find any merit in the contention of the Ld. Counsel for the assessee that the decision of the Special Bench in Instrumentarium (supra) is distinguishable on facts and hence not applicable in the impugned year in the case of assessee.

We find the argument of the Ld. Counsel for the assessee itself to be incorrect that in the case of Instrumentarium (supra) the base erosion argument of the assessee was adjudicated against the assessee taking note of the fact that the AEs were incurring losses, and therefore, there was no base erosion happening on account of ALP adjustment made to the international transaction in the hands of the assessee.

15. We have noted that this identical argument was made by the assessee before the TPO who also had rejected the same noting that the Special Bench in the case of Instrumentarium (supra) had laid down a proposition of law that the concept of there being base erosion on account of the ALP of foreign entity undergoing an upward adjustment was incorrect. We are in complete agreement with the TPO on this count.

16. We have also gone through the order of the Special Bench in the case of Instrumentarium (supra) and we find that it has in principle laid down that there is no base erosion by the ALP adjustment in the hands of the non-resident company in respect of transaction with the Indian AEs. Para-15 to 19 of the order of the Special Bench specifically and categorically deal with the arguments of the base erosion theory propounded by the assessee.

17. The assessee in principle had argued that there is no erosion of tax base in India by the assessee foreign entity by charging lesser amount for services. That on the contrary an upward ALP adjustment to the transaction in the hands of the foreign entity (the assessee in the present case) would result in base erosion, since the adjustment would result in lesser taxes being collected on the impugned transaction collectively both from the foreign entity and its Indian AE. The logic forwarded by the assessee before the Special Bench was that the foreign entity was liable to tax at the rate of 10% in terms of provisions of DTAA for the receipts from its Indian AE, while the Indian AE was subjected to tax at the rate of 33.75%; that any upward adjustment in ALP of the international transaction of the foreign assessee would result in a corresponding adjustment to the corresponding transaction carried out by the Indian AE, resulting in its expenses increasing to that extent, reducing taxable profits accordingly. The net effect would be that while there would be a gain of 10% taxes on the TP adjustment made, there would also be a corresponding loss of 26.75% taxes on account of the ALP adjustment in the hands of Indian AE. The assessee’s argument was based on the interpretation of provision of section 92(3) read with section 92C(4) of the Act.

18. The Special Bench, however, rejected outright this contention of the assesse, noting that in terms of provision of law, any adjustment to the ALP of the international transaction of a foreign entity did not warrant an adjustment in ALP of its Indian AE also. The Special Bench categorically noted that the deduction for the ALP adjustment will not be available to the Indian AE, because there is no provision enabling deduction for the ALP adjustment. The assessee had referred to second provision to section 92C(4) for stating that in terms of second proviso, the Indian AE was not debarred from making the corresponding adjustment in ALP of the transaction, and this contention of the assessee was also rejected by the Special Bench, noting that second proviso to section 92C(4) of the Act constituted a bar against lowering of the income of the non-resident AE as a result of lowering the deduction in the hands of the Indian AE, rather than as enabling higher deduction in the hands of Indian AE, as a result of increasing non-residents AE income. This finding of the Special Bench are categorically noted in para 19 of the order as under:

“19. A plain reading of Section 92(3), however, indicates that what is to be seen is impact on profits or losses for the year in consideration itself as it is to "be computed on the basis of entries made in the books of accounts in respect of previous year in which the international transaction was entered into". There is thus no scope at all for taking into account the impact on taxes for the subsequent years. The tax shield available to the assessee's AE, as a result of accumulated losses- even if any, can only affect the income of the subsequent years, which, for the reasons noted above, are not relevant for the purpose of Section 92(3). The manner in which the argument of the assessee is placed, a part of the section is being interpreted in isolation without appreciating the impact of the other part of the same section. Such an approach is clearly not permissible. This legal position apart, the arguments of the assessee also proceed on the fallacious logic inasmuch as the amount by which income of the assessee is increased by the arm's length price adjustments, under the Indian law, is not available for deduction in the hands of the corresponding Indian AE. Take for example a situation in which the assessee has not earned an income of Rs 100 from interest on account of loan given by the assessee to its Indian AE, or from fees for technical services rendered to the Indian assessee, but an ALP adjustment of Rs 400 is made in respect of this income. In such a situation, what is deductible in the hands of the Indian AE is only Rs 100 and not Rs 500. Therefore, as a result of this ALP adjustment, there is no lowering of profit or increase in loss of the AE even while income of the assessee stands increased by Rs 400. There is no base erosion by the ALP adjustments in the hands of income of the non-resident company in respect of transactions with the Indian AEs. The base erosion could have, if at all, taken place at best in a situation in which the Indian AE was to actually allow the income to the non-resident company. That is not the case before us, and in such a situation, in any event, ALP adjustments would not have come into play at all. As regards learned counsel's contention that if there is an enhancement to an income corresponding deduction cannot indeed be given to the related AE, but if an altogether new income is brought to tax in the hands of the assessee, as a result of ALP adjustment, corresponding deduction is required to be given to the Indian AE, we find no basis whatsoever for this contention. The scheme of transfer pricing legislation does not support the plea of the assessee. Learned counsel has not been able to point out any specific legal provision enabling such a corresponding deduction or demonstrate, or even remotely suggest, the line of demarcation as visualized by the learned counsel. As regards the reference to second proviso to Section 92C(4) made by the learned CIT(A), on incorrectness of which so much reliance has been placed by the learned counsel, the CIT(A) was indeed in error as it refers to re-computation of income in the hands of an AE, as a result of lower deduction being allowed, but then nothing really turns on that. The reasoning given by the CIT(A) was incorrect, the conclusion arrived at him by was not. He was right, even if serendipitously. The deduction for the ALP adjustment will not be available to the Indian AE because there is no provision enabling deduction for ALP adjustments. The second proviso to Section 92C(4) refers to a situation in which let us say an a resident assessee paid Rs 100 for interest to its AE abroad, and duly deducted tax from the same or the tax was deductible from the said payment, but the arm's length price of the interest was ascertained at Rs 40. In such a situation, while deduction, as per arm's length principle, is to be allowed only for Rs 40, the taxability in the hands of the AE shall continue to be for Rs 100. Clearly, therefore, reference to second proviso to Section 92C(4), as made by the learned CIT(A), was wholly unwarranted. However, learned counsel of the assessee is also equally in error when he contends that since the second proviso to Section 92C(4) does not come into play on the facts of this case, "there is nothing in the Act which prohibits Datex (i.e. Indian AE) to recompute its income and claim the loss to be set off against the profits of the future years". In fact, nothing in the Income Tax Act enables such a claim of deduction. As for second proviso to Section 92C(4), it constitutes a bar against lowering income of the non-resident AE, as a result of lowering the deduction in the hands of the Indian AE, rather than as enabling a higher deduction in the hands of the Indian AE as a result of increasing non-resident AE's income.

Therefore, it is clearly evident that the Special Bench had not rejected the base erosion argument of the assessee on any factual basis/consideration of the Indian AE incurring losses but rather had held so as a matter of principle. We hold that the Special Bench in the case of Instrumentarium (supra) has laid down principle of law to the effect that there is no base erosion by ALP adjustment in the income of the non-resident in respect of its transactions with the Indian AEs.

19. In view of the above we reject this argument of the ld. counsel for the assessee that the decision of the Special Bench in the case of Instrumentarium (supra) rejecting the base erosion argument of the assessee would not apply in the facts of the present case.

20. The ld. counsel for the assessee, thereafter pointed out that in the preceding year, it had raised an argument, regarding Benefit of Treaty (DTAA) against applicability of TP provisions in reference to Article 9(1) of the India Netherlands Tax Treaty . The ld. counsel for the assessee fairly conceded that this argument of the assessee had been rejected by the ITAT in its order in the case of the assessee for Asst.Year 2007-08 to 2010-11. This argument of the assessee, therefore, is also dismissed.

21. Next argument raised by the Ld. Counsel for the assessee was regarding the principle of mirror ALP. The argument of the ld. counsel for the assessee was that, if the ALP of a transaction with one of the AE’s to an international transaction is determined, the same ALP is to be applied with respect to other AE also. In fact the specific argument of the ld. counsel for the assessee was that in the case of Indian AEs of the assessee i.e. “HLPL” and “SIMPL”, the ALP of the transaction entered into with the assessee had been determined by the TPO and accepted at the Price at which it was recorded by the assessee. Having done so, there was no cause of action now with the TPO of the assessee to make any adjustment in the hands of the assessee. This, in substance, was the “mirror ALP” argument of the ld. counsel for the assessee.

22. The ld. counsel for the assessee stated that identical argument had been raised before the ITAT in the case of the assessee in Asst. Year 2011-12 and 2013-14, but the same had been rejected by the ITAT; that the assessee had filed an MA against the said ruling of the ITAT, which was also dismissed by the ITAT. The ld. counsel for the assessee contended that the ITAT, in fact, had dismissed the assessee’s mirror ALP argument holding that it would be applicable only in the circumstances viz.

(i) a TP reference is made in the case of AE,

(ii) a TP assessment is undertaken in the case of AE, and

(iii) no TP adjustment made in the case of the AE.

23. The ld. counsel for the assessee contended that in the present case there were orders of the TPO both in the case of “SIMPL” and “HLPL”, where the TPO had accepted the ALP of the transaction entered by the Indian AE with the assessee. He, therefore, stated that in terms of the order of the ITAT in the preceding year, i.e. Asst. Year 2011-12 to 2013-14, the assessee’s argument on mirror ALP should find favour in the impugned year, and the ALP adjustment made, therefore, be deleted.

24. We have heard the ld. counsel for the assessee, and we do not find any merit in the contentions of the ld. counsel that the ALP adjustment should be deleted by applying the principle of mirror ALP. We have gone through the order of the ITAT in the case of the assessee for Asst. Year 2011-12 to 13-14 and have noted that it had referred to the decision of the ITAT, Bangalore Bench in the case of Filtrex Technologies P. Ltd. Vs. ACIT, 93 taxmann.com 301 (Bangalore- Tribunal) while rejecting the mirror ALP argument.

25. We have perused the order of the ITAT in the case of Filtrex Technologies P.Ltd. (supra) and we note in the said case that the ITAT has categorically held that in terms of provision of law relating to TP, there could not be any case of mirror ALP at all. The ITAT, referred to the decision of Special Bench in the case of Instrumentarium (supra) and noted that in the said case, the Special Bench has categorically held that the ALP adjustment in the case of one AE does not automatically warrant a corresponding adjustment in the hands of the other AE in terms of TP provision, as enacted in our Statute. The ITAT analyzed the relevant provisions of law, more particularly section 92(3) and second proviso to section 94CA(4) of the Act, and applying the ratio laid down by the Special Bench of the ITAT in the case of Instrumentarium Corpn. Ltd. (supra) held that in respect of a same transaction the Revenue can opt to determine total income on the basis of ALP determined in accordance with section 92(1) of the Act in the hands of one party to the said transaction, wherever tax base would erode and can desist from doing so in the assessment of the other party to the said transaction wherever there would not be tax base erosion. That therefore it cannot be said that consequent to acceptance of return of income filed by one party to the transaction, the price paid by the other party in the international transaction has to be accepted as at Arms Length. The relevant findings of the ITAT are reproduced at para 28 & 29 of its order as under;

“28. It is clear from the above circular that second proviso to Sec. 94CA(4) is meant to apply only when ALP is determined in the case of FIPL and FHPL. Another aspect which the Circular makes it clear is that the commercial reality of a transaction will be looked into viz., wherever the determination of income or expense in the hands of one enterprise results in tax base erosion of the country, the AO is free to apply the provisions of Sec.92(1) read with Sec.92CA(4). Corresponding adjustment in the assessment of the other enterprise to the transaction need not be made where there is no tax base erosion of the country. This is also the purport of Sec.92(3) of the Act which lays down that wherever computation of income under sub-section (1) of Sec.92 or the determination of the allowance for any expense or interest under that sub-section, or the determination of any cost or expense allocated or apportioned, or, as the case may be, contributed under sub-section (2) of Sec.92, has the effect of reducing the income chargeable to tax or increasing the loss, as the case may be, computed on the basis of entries made in the books of account in respect of the previous year in which the international transaction was entered into. There would appear to be a conflict between the provisions of Sec. 92CA(4) and Sec.92(3) but a harmonious construction of these provisions would be hold that in respect of a same transaction the revenue can opt to determine total income on the basis of ALP determined in accordance with Sec.92(1) of the Act, in the hands of one party to the said transaction, wherever tax base of the country would erode. The revenue can desist from doing so in the assessment of the other party to the said transaction wherever there would not be tax base erosion. It cannot therefore be said that consequent to acceptance of return of income filed by FHPL and FIPL, the price paid by the Assessee in the international transaction has to be accepted as at Arm's Length.

29. In the light of the above discussion and the decisions on the issue rendered after the decision in the case of UE Development India Pvt. Ltd. (supra), we are of the view that ALP has to determined in the hands of the Assessee irrespective of the acceptance of ALP in the hands of FHPL and FIPL. The question as to whether the payment for such services are at Arm's Length or commensurate with the benefit received by the Assessee are all matters which needs examination by the TPO. No such exercise has been carried out by the TPO. But that does not mean that the ALP has been established by the Assessee. We are therefore of the view that it would be just and proper to set aside the order of the Assessing Officer on this issue and remand the question of determination of ALP to the TPO for fresh consideration. It is made clear that the TPO shall not dispute that services were rendered by the AE. If the approach of the Assessee in adopting TNMM at entity level is disputed by the TPO, the Assessee should be permitted to file TP study for each of the international transaction separately. The assessee is also directed to file the TP study, if not already filed which is in accordance with the provisions of the Act and substantiate that the price paid by it to its AE is at arm's length within the methods laid down in the Act and the judicial decisions rendered on this issue. The TPO will consider the same in accordance with the law, after affording an opportunity of being heard."

26. As regards reference to the earlier year decision in the case of the assessee by the Ld. Counsel for the assessee where the decision was stated to be made on the basis of facts of the case of there being no TP reference made in the case of the AE, the same merits no consideration in view of the proposition of law laid down in this regard by the ITAT in the case of Filtrex (supra).

27. We have also noted that in the Miscellaneous application filed by the assessee against the said order of the ITAT in A.Y 2011-12 to A.Y 2013-14, the mistake pointed out was the reliance placed by the ITAT on the decision of ITAT Bangalore Bench in the case of Filtrex (supra), when the assessee had referred to the decision of the Hon’ble Karnataka High Court in the case of UED India Pvt. Ltd in support of its legal argument of Mirror ALP. Though the ITAT while dismissing the MA found no merit in the Mirror ALP argument on the facts of the case before it, but we find that the decision of the Hon’ble Karnataka High Court is of no assistance to the assessee.

Copy of the decision of the Hon’ble High Court and also the ITAT in the case of UED India(supra) was filed before us. The specific citations of both are as under:

i) UE Development India Pvt. Ltd v. DCIT- IT(TP)A No. 284 to 286/Bang/2012 & 1104/Bang/2011- dated 30-Aug-2013;

ii) UE Development India Pvt Ltd v. DCIT - ITA NO. 1506/BANG/2012- Dated 14 July 2017;

iii) CIT v. UE Development India Pvt. Ltd. - ITA No. 52/2014 - dated 12 July 2018 - Karnataka High Court;

iv) CIT v. UE Development India Pvt. Ltd. - ITA No. 53/2014 - dated 12 July 2018 - Karnataka High Court;

v) CIT v. UE Development India Pvt. Ltd. - ITA No. 54/2014 - dated 12 July 2018 - Karnataka High Court;

vi) Development India Pvt. Ltd. - ITA No. 55/2014 - dated 12 July 2018 - Karnataka High Court “

28. The ITAT in its decision in UED (supra) ruled in favour of the assessee. When the matter travelled to the Hon’ble High Court, the question of law framed before it was -

"Whether on the facts and in the circumstances of the case the Tribunal is right in law in holding that in mirror transactions ALP adjustments cannot be done, i.e., if one transaction is treated as at Arm's Length, no adjustment can be made on the other related corresponding transaction of the AE without appreciating that this stand is against the provisions of Section 92(3) of the Act ?"

To which the High Court dismissed Revenues appeal stating that no substantial question of law arose in the case following its order in the case of M/s Soft brands India Pvt. Ltd. in ITA No. 536/2015 c/w 537/2015 dated 25-06-2018, wherein it held that mere dissatisfaction with the findings of facts arrived at by the ITAT is not at all a sufficient reason to invoke section 260A of the Act before the High Court.

29. The Hon’ble High Court decision in the case of UED (supra) being rendered in the facts of the case, it cannot be said to be laying down any proposition of law. And therefore no benefit whatsoever can be derived by the assessee from the said decision.

In view of the above discussion the Mirror ALP argument of the assessee also stands rejected following the decision of the ITAT in the case of Filtarex (supra).

30. The ld. counsel for the assessee, thereafter, stated that his next contention with respect to the adjustment made to the ALP of the transaction in the hands of the assessee was that the CUP method had not been correctly applied. He stated that this argument was applicable only to the international transaction with AE HLPL and not with SIMPL.

He pointed out that in the preceding years i.e. Asst.Year 2011- 12 to 2013-14, this point had been raised before the Tribunal for the first time, contending that while the TPO had picked up Brunei LNG., as a comparable for applying CUP method, it had failed to make the comparison correctly. He contended that they were two components to the services provided by the assessee-company viz. one of fixed component and other of optional/variable component; that this structure of payment was there in the case of Brunei LNG also; that while making comparison, the TPO ought to have compared the fixed services charges collected by the assessee with that collected by the Brunei LNG and optional service charges collected with that by Brunei LNG, but the TPO had not done so. He contended that the ITAT had appreciated the argument and restored the matter back to the TPO to make a fresh comparative analysis. In this regard, he drew our attention to the argument on this line before the ITAT page no.8 of the order as under:

“4. ….. Further, it was submitted before us that the assessee has rendered services with respect to LNG storage and re-gasification terminal to its AEs i.e. HLPL and HPPL. Similar services were also provided to third parties i.e. BLNG. The Counsel for the assessee submitted that the structure of these two contracts i.e. the Operating Services Agreement (OSA) with HLPL and HPPL as well as with BLNG are structured in a similar manner i.e. there is a fixed component of services along with annual quota of entitlements are for which there is a lumpsum annual fee and there is a provision to provide various optional services which would be invoiced basis the charged out rates for the employees under various job groups. However, it was submitted that the TPO has erred in quantification of TP adjustment i.e. fixed services have not been compared with fixed services and optional services have not been compared with optional services. Hence, it was submitted that "likes have not been compared with likes" and the assessee placed reliance on the decision rendered by ITAT Hyderabad in the case of M/s. Takshill Solutions Ltd. in ITA No. 1768/Hyd/2012 where in the same principle of "likes have not been compared with likes" has been adjudicated.”

31. He thereafter drew our attention to the finding of the ITAT appreciating arguments of the assessee, and restoring the issue back to the TPO for fresh comparability analysis, as at para 7 of the page no.17 of the order as under:

“7. …… Further, we observe that the argument of "likes have not been compared with like" and the argument of similarity of agreement with BLNG were never taken before the Tax Authorities at any stage of the hearing. Accordingly, looking into the facts of the instant case, and respectfully following the decision rendered by ITAT Bangalore in the case of Filtrex Technologies Pvt. Ltd. (supra), the matter is being restored to the file of Ld. AO for determination of ALP in respect of the aforesaid transactions. The assessee is also directed to file the relevant supporting documents to substantiate that the price paid by the AEs to the assessee is at arm's length within the methods laid down in the Act and the judicial precedents rendered on this issue. The Ld. TPO is directed to consider the same in accordance with the law, after affording an opportunity of being heard to the assessee.”

32. He, therefore, contended that in the impugned order also identical direction be given to the TPO.

The ld. DR fairly agreed to the same.

33. In view of the above therefore, the TPO is directed to determine the ALP in respect of the impugned international transactions with HLPL afresh after making a proper TP analysis in accordance with the direction of the ITAT in the preceding year as noted above.

34. Next argument raised by the ld. counsel for the assessee before us was that the income received by the assessee on account of rendering of services was taxable in the source country only on receipt basis. His contention was that since the adjustment made to the ALP of the transaction was not received, the same was not taxable, therefore, there was no occasion for making any ALP adjustment. He fairly conceded that this issue is pending before the Special Bench of the ITAT in the case of Ampacet Cyprus Ltd(ITA 1518/Mum/2016 and ITA 560/Mum/2017. It was pointed out that vide order sheet entry dated 10/11/23 the Special Bench had sent the reference back to the ITAT President for reformulating the questions. It was therefore pleaded that the matter be restored back to the AO to adjudicate it after applying the decision of the Special Bench on the issue as and when decided.

The ld. DR fairly agreed with the same.

35. In the light of the same, we restore the issue back to the AO with the direction to apply the decision of the Special Bench on the issue of applicability of ALP adjustment to receipts which are otherwise not taxable in terms of provisions of DTAA as argued by the assessee before us. He shall consider the facts of the case and give due opportunity of hearing to the assessee while doing so.

In effect ground No.1 is partly allowed for statistical purposes for a fresh comparability exercise in the transaction with HLPL and for applying the decision of the Special Bench on the issue of TP provisions being applicable even where the adjustment made to income of AE is not liable to be taxed in terms of the DTAA agreement.

36. Ground No.2 raised by the assessee reads as under:

“2. Income from software treated as royalty in nature - INR 28,68,584

The learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in treating the revenues of INR 28,68,584 received by the Appellant from Bharat Oman Refineries Limited ('BORL') and Bharat Petroleum Corporation Limited ('BPCL') for grant of software license as royalty under section 9(l)(vi) of the Act and under Article 12 of DTAA.

37. The ld. counsel for the assessee stated that the issue stands covered by the decision of the ITAT in Asst. Year 2011-12 to 2013-14. He stated the issue related to the treatment of payment received for supply of software license to the entities as under, treated as royalty by the AO under section 9(1)(vi) read with the applicable Treaty:

|

i) |

Bharat Oman Refiners Ltd. (BORL) |

: Rs.9,89,167/- |

|

ii) |

Bharat Petroleum Corpn Ltd. (BPCL) |

: Rs.18,79,417/- |

|

|

|

Rs.28,68,584/- |

38. The ld. counsel for the assessee stated that the DRP had dismissed the assessee’s objection to the proposed treatment, by following its order for Asst. Year 2011-12. He pointed out that the issue had travelled to the ITAT in Asst.Year 2011-12 and the ITAT had ruled in favour of the assessee holding such payment did not qualify as Royalty, following the decision of the Hon’ble Supreme Court in the case of Engineering Analysis Centre of Excellence P. Ltd., 125 taxmann.com 42 (SC). Our attention was drawn to para 11 to 12 of the order of the ITAT in Asst. Year 2011-12 as under:

“11. The brief facts in relation to this ground of appeal are that the assessee earned revenues from provision of off the shelf standard software to certain Indian entities. The Assessing Officer taxed the aforesaid amounts as software royalty in the hands of the assessee under Section 9(1)(vi) of the Act read with the applicable Treaty law. While holding receipts as royalty payment, the DRP primarily relied upon the decision of Karnataka High Court in the case of CIT vs. Samsung Electronics Co. Ltd. 16 taxmann.com 141 to hold that the payments received by the assessee company from Indian customers give rise to royalty income in terms of Article 12 of India- Netherlands DTAA r.w.s. 9(1)(vi) of the Act.

12. Before us at the outset, the Ld. Counsel for the assessee submitted that now the taxability of software royalty has been decided in favour of the assessee by the decision rendered by the Hon'ble Supreme Court in the case of Engineering Analysis Centre of Excellence Pvt. Ltd. 125 taxmann.com 42 (SC) and also in the Supreme Court decision in the case of Infosys Technologies Ltd. 142 taxmann.com 224 (SC). We observe that the Hon'ble Supreme Court in the aforesaid decisions have held that amount payments by resident Indian and user / distributors to non-resident computer software manufacturers / suppliers as consideration for resale / use of computer software through distribution agreement is not payment for use of copy right in computer software and thus, same does not amount to income taxable in India. Accordingly, in view of the aforesaid decision, wherein the Hon'ble Supreme Court has held that payments made the assessee to non-resident related to use of computer software was not royalty, this issue is decided in favour of the assessee.”

39. He, therefore, stated that the impugned addition made by the AO be deleted.

The ld. DR fairly conceded to the same.

40. In view of the above, since admittedly the above issue is covered in favour of the assessee by the decision of the ITAT on the identical issue for Asst. Year 2011-12, the addition made to the income of the assessee by treating the receipts on account of supply of software licence, as royalty to the tune of Rs.28,68,584/- is deleted.

Ground no.2 is allowed.

41. Ground no.3 reads as under:

“3. Income from rendering Global P&T Functional Services treated as fees for technical services - INR c The learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in treating the revenues of INR 87,46,96,276 received by the Appellant from SIMPL for Global P&T Functional Services as Fees for technical services under section 9(l)(vii) of the Act and under Article 12 of DTAA.

3.2. Without prejudice to above mentioned Ground No. 3.1, the learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in disregarding the fact that amount received for the above mentioned services is mere reimbursement of expenses incurred by the Appellant without any mark up and hence is in the nature of reimbursement of expenditure.”

42. At the outset itself, ld. counsel for the assessee contended that the issue raised in the ground 3.1 stood covered in favour of the assessee by the decision of the ITAT in Asst.Year 2012-13 in ITA NO.747/Ahd/2017 dated 11.10.2023. He pointed out that the issue related to the treatment of service rendered by the assessee to its subsidiary “SIMPL” for providing Global P&T Functional services as fee for technical services under section 9(1)(vii) of the Act read with applicable Tax Treaty. The services included providing strategy support services, human resources services, legal services, providing advice relating to environmental healthy and safety matters and provision of IT services etc. The AO has treated the same as in the nature of “fee for technical services” and subjected to tax in India under section 9(1)(vii) of the Act read with Tax Treaty. The objection of the assessee to the DRP against the same was dismissed following its decision for earlier years.

43. The ld. counsel for the assessee pointed out that identical addition made in the hands of the assessee in Asst. Year 2012-13 was decided in favour of the assessee, dealt with by it at para 36 to 40 of its order as under:

“36. The assessee has raised the following grounds of appeal: -

"3. Income from rendering of Global P&T Functional Services treated as fees for technical services - Rs. 15,58,83,228

3.1. The learned AO/TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO/IPO on the facts and in law in treating the revenues of Rs 15,58,83,228 received by the Appellant from Shell India Markets Private Limited (SIMPL) for Global P&T Functional Services as Fees for technical services under section 9(1)(vii) of the Act and under Article 12 of DTAA.

3.2. Without prejudice to above mentioned Ground No. 3.1 above, The learned AO/TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO/FPO on the facts and in law in disregarding the fact that amount received for the above mentioned services is mere reimbursement of expenses incurred by the Appellant without any mark up and hence is in the nature of reimbursement of expenditure."

37. During the year under consideration, the assessee entered into an agreement with it's subsidiary Shell India Pvt. Ltd. to provide Global P&T Functional Services. Broadly, the services included proceeding strategy support services, human resources services, legal services, providing advice relating to environmental healthy and safety matters and provision of IT services etc. The Assessing Officer treated the above services as "Fee for Technical Services" under Section 9(1)(vii) of the Act read with the Tax Treaty. The aforesaid additions were also confirmed by DRP.

38. The assessee is in appeal before us against the aforesaid order passed by DRP holding that the aforesaid services qualify as "Fee for Technical Services" and are hence taxable in India. Before us, the Counsel for the assessee submitted that in view of the "make available clause" under the India- Netherlands Tax Treaty, payments for such services do not quality as FTS since the assessee has not made available any technical knowledge, experience, skill, know-how or process to Shell India and hence the same are not taxable as FTS under Article 12 of the Tax Treaty. Further, it was submitted that the above services are provided by the assessee on recurring basis from year to year and if the technology had been "made available" to its subsidiary Shell India, there would have been no need for availing the aforesaid services on a recurring basis, from year to year. Accordingly, it was submitted that the aforesaid services do not qualify as FTS under the India-Netherlands Tax Treaty.

39. In response, the Ld. D.R. placed reliance on the observation made by the Assessing Officer in his order.

40. We have heard the rival contention and perused the material on record. On going through the nature of services, we are of the considered view that the aforesaid services do not qualify as fee for technical services in view of the specific exclusion provided under the India-Netherlands Tax Treaty excluding those services from the ambit of technical services, which do not "make available" technology to the recipient of such services. On perusal of the nature of services, in our considered view, no such technology has been made available to Shell India during the course of rendering of such services. From the facts placed before us it is evident that the Department has not been able to substantiate that the services were rendered in a manner so as to make the technology available to the recipient of services in a manner that in the future the recipient is able to perform the aforesaid services, without further recourse to the services of the assessee. In the recent case of Star Rays 153 taxmann.com 226 (Gujarat) the Gujarat High Court held that where assessee company availed diamond testing services for certification of diamond from U.S. company and claimed that payment was not tax deductible at source, assessee's case was protected under India-USA DTAA as mere rendering of services could not be roped into FTS since assessee company utilising services was unable to make use of technical knowledge etc. of AE. While passing the order, the Gujarat High Court made the following observations:-

"6. Apparently reading the orders under challenge would indicate that based on factual appreciation especially the condition in the customer service agreement, the bank invoice and the Bank remittance advice a finding of fact has been arrived at that the assessee's case was protected under the India- USA DTAA and that mere rendering of services cannot be roped into FTS unless the person utilising the services is able to make use of the technical knowledge etc. Simple rendering of services as in the present case is not sufficient to qualify as FTS."

41. Accordingly, in view of the facts of the assessee's case and the judicial precedents on the subject which have consistently taken a view that unless the services are rendered in the manner such that the technology is "made available" transferred to the assessee in such a manner that he is enabled to perform such services by itself in the future and does not require further services from the service provided, it is only then that such services would qualify as fee for technical services under the applicable Tax Treaty which specifically contains the "make available" clause. In the instant facts, we observe that nature of services are not which make available the technology to the recipient of services i.e. Shell India and further, the Department has also not placed on record any evidence to support that such services have made available the technology to the recipient of such services.”

44. Ld. DR fairly agreed with the same.

45. In view of the above, since admittedly the above issue is covered in favour of the assessee by the decision of the ITAT on the issue for Asst. Year 2012-13,the addition made to the income of the assessee by treating the receipts on account of service rendered by the assessee to its subsidiary “SIMPL” for providing Global P&T Functional services as fee for technical services under section 9(1)(vii) of the Act, amounting to Rs.87,46,96,276/-, is deleted.

Ground no.3.1 is allowed.

46. The ld. counsel for the assessee thereafter pointed out that in ground No.3.2 an alternate argument had been raised by the assessee with respect to the issue of treatment of amount received from SIMPL for rendering Global P&T Functional services as fee for technical services. The assessee’s alternate contention was that it was merely in the nature of reimbursement , and therefore also not liable to be subjected to tax. He pointed out that the ITAT in the preceding year had not adjudicated this ground since the assessee’s plea against the treatment of the impugned amount as fee for technical services, had been accepted.

The ld. DR fairly conceded to the same.

47. In view of the above, since, we have also treated this amount received by the assessee from SIMPL of Rs.87.46 crores as not liable to be taxed as FTS in ground no.3.1 raised by the assessee in paraITA 45 of our order above, we do not consider it necessary to deal with the alternate ground raised by the assessee.

Ground No.3.2 is, therefore, not being dealt with by us.

48. Ground No.4 reads as under:

“4. Income from HLPL treated as fees for technical services - INR 8,74,34,868

4.1. The learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in treating the revenues of INR 8,74,34,868 received by the Appellant from HLPL as Fees for technical services under section 9(l)(vii) of the Act and under Article 12 of DTAA.

4.2. Without prejudice to above mentioned Ground No. 4.1, the learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in disregarding the fact that amount of INR 2,42,157 received from HLPL (under Contract No. 138975) is mere reimbursement of expenses incurred by the Appellant without any mark up and hence is in the nature of reimbursement of expenditure.”

49. The issue raised in this ground was also stated by the ld. counsel for the assessee to be covered in favour of the assessee by the decision of the ITAT in the immediately preceding year i.e. Asst.Year 2012-13 and 2013-14. The issue, he contended, related to treatment of certain services rendered by the assessee to Hazira LNG Pvt. Ltd. (HLPL), Hazira Port P. Ltd., and HPCL as fee for technical services under section 9(1)(vii) of the Act and also under Article 12 of the DTAA. The assessee had provided Computational Fluid Dynamics (CFD) modelling of the temperature effects on the Hazira sea water outflow into the port and also provided marine biological advice on its implication to HLPL. The assessee has also provided desktop quality review of Shell Reliability Centre Maintenance done by HLPL. The assessee had performed integrity review of ageing switchgear and had received in all a total consideration of Rs.8,74,34,868/-. The AO had treated the entire service as fee for technical services under section 9(1)(vii) of the Act read with Article 12 of the DTAA and the DRP had dismissed the assessee’s objection to the same, following its order in the immediately preceding years i.e. Asst. Year 2013-14. The ld. counsel for the assessee pointed out that the identical issue had come up before the ITAT in Asst. Year 2012-13 and the issue had been decided in favour of the assessee by the ITAT. He drew our attention to para-15 to 19 of the order in this regard as under:

“15. The assessee has raised the following grounds of appeal:

"3. The learned AO based on the directions of the DRP has erred on the facts and in law in treating the revenues of Rs. 51,68,025 received by the Appellant from Hazim LNG Port Limited, Hazira Port Private Limited and Hindustan Petroleum Corporation Limited as Fee for technical services under section 9(1)(vii) of the Act and under Article 12 of Tax Treaty."

"4. Income from HLPL treated as fees for technical services - Rs.2,84,20,716 The learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in treating the revenue of Rs. 2,84,20,716 received by the Appellant from HLPL as Fees for technical services under section 9(1)(vii) of the Act and under Article 12 of DTAA."

16. The brief facts in relation to these grounds of appeal are that the assessee provided Computational Fluid Dynamics (in short "CFD") modelling of the temperature effects on the Hazira Sea Water outflow into the port and also provided marine biological advice on its implications to HLPL. Further, the assessee provided desktop quality review of Shell Reliability Centre Maintenance done by HLPL's site team. Further, the assessee performed a Integrity Review of Ageing Switchgear (in short "IRAS") for HPCL for providing the above services, and the assessee received a total consideration of Rs. 51,68,025/-. The Assessing Officer held that the aforesaid receipts qualify as fee for technical services under Section 9(1)(vii) of the Act read with Article 12 of the Treaty.

17. Before us, the primary argument taken by the Ld. Counsel for the assessee that under the applicable India-Netherlands treaty, the taxability of aforesaid services are governed by the "make available" clause in respect of payment for "Fees for Technical Services (FTS)", in terms of which payments for services qualify as FTS under the Income Tax Act read with the India- Netherlands Treaty only if the assessee "makes available" technology to the recipient of services. It was submitted that in the instant facts while holding that aforesaid payments as FTS, nothing has been brought on record by the Department to demonstrate that the condition of "make available" as provided under the Treaty has been satisfied in the instant set of facts, so as to make the payment taxable in India as FTS.

18. In response, Ld. D.R. placed reliance on the observations made by DRP in its order.

19. We have heard the rival contention and perused the material on record. On going through the description of services, perusal of the relevant agreements and the order passed by the DRP, we are of the considered view that looking into the nature of services there is nothing to suggest that the condition of "make available" as provided in the India-Netherlands Tax Treaty have been satisfied. Further, looking into the nature of services, there is nothing to suggest that there was any agreement for transfer of any technical plan or design to the recipient of services under the aforesaid agreement as well. Further, looking into the nature of services, wherein the analysis done by the assessee is submitted in a form of report to the recipient of services, there seems to be nothing to suggest that the technology for providing the aforesaid services have been imparted to the recipient of services in a way that the recipient of services would not be required the services of the assessee further in the future and has been enabled by the assessee to perform such services on its own without any recourse or assistance of the assessee in the future. More specifically, with respect to Work Order No. 131965, we observe that the work performance on the analysis was done only with a view to advice HPCL to decide whether switchgear was obsolete and hence, required to be refurbished or replaced. Therefore, looking into the instant facts we are of the considered view that the condition of "make available" has not been satisfied in the instant set of facts and hence, the services do not qualify as FTS. In this connection it would be useful to reproduce the relevant extracts of the decision of Karnataka High Court in the case of CIT vs. De Beers Indian Minerals Pvt. Ltd. 21 taxmann.com 214 (Kar.):-

"Therefore, the assessee not being possessed with the technical know how to conduct this prospecting operations and reconnaissance operations, engaged the services of Fugro which is expert in the field. By way of technical services Fugro delivered to the assessee the data and information after such operations. The said data is certainly made use of by the assessee. Not only the said data and information was furnished in the digital form, it is also provided to the assessee in the form of maps and photographs. These maps and photographs which were made available to the assessee cannot be construed as technology made available. Fugro has not devised any technical plan or technical design. Therefore, the question of Fugro transferring any technical plan or technical design did not arise in the facts of these cases. The maps which are delivered are not of kind of any developmental activity. As such, earlier the information which is furnished to the assessee by way of technical services in the digital form is also given in the form of maps. Therefore, the case on hand do not fall in the second part of the aforesaid clause dealing with development and transfer of plans and designs."

50. The ld. DR fairly agreed to the same.

51. In the light of above discussion, since the above issue is admittedly covered in favour of the assessee by the decision of the ITAT on the issue for Asst.Year 2012-13 the addition of Rs. 8,74,34,868/- on account of receipt from HLPL as fees for technical services made to the income of the assessee is deleted.

Ground no.4 is allowed.

52. Ground No.5 reads as under:

“5. Income from Larsen & Toubro Limited ('L&T') treated as fees for technical services - INR 73,92,399/-

5.1. The learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in treating the revenue of INR 73,92,399 received from L&T as taxable under section 9(l)(vii) of the Act.

5.2. Without prejudice to above mentioned Ground No. 5.1, the learned AO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in disregarding the contention of the Appellant that the services provided to L&T do not make available any technical knowledge, experience, skills, know how etc. and also do not consist of the development and transfer of technical plan or technical design and therefore do not qualify as FTS under Article 12 of the DTAA.”

53. This issue also, it is stated, had been decided in favour of the assessee by the ITAT in Asst. Year 2011-12. He contended that the issue related to the treatment of income received from L&T services, as fee for technical services under section 9(1)(vii) of the Act, amounting to Rs.73,92,399/-. The ld. counsel for the assessee contended that identical issue was adjudicated by the ITAT in Asst. Year 2011-12 in favour of the assessee vide para 22 to 28 as under:

“22. The assessee has raised the following grounds of appeal:-

"4. The learned AO based on the directions of the DRP has erred on the facts and in law in treating the revenues of Rs. 8,18,82,400 received from Larsen & Toubro Limited ('L&T') as taxable under section 9(1)(vii) of the Act."

4. Income from Larsen & Toubro Limited ('L&T') treated as fees for technical services

The learned AO/TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO/TPO on the facts and in law in treating the revenue of Rs. 7,41,84,000 received from L&T as taxable under section 9(1)(vii) of the Act."

"5. Income from Larsen & Toubro Limited ('L&T') treated as fees for technical services - Rs. 2,44,01,667

The learned AO/TPO has erred on the facts and in law and learned DRP has further erred in confirming the action of the AO on the facts and in law in treating the revenue of Rs. 2,44,01,667 received from L&T as taxable under section 9(1)(vii) of the Act."

23. The brief facts in relation to these grounds of appeal are that the assessee had entered into the several contracts with Larsen & Toubro (in short "L&T") in connection with L&T's various projects outside India. The services broadly included engineering services related to manufacturing of coal gasification equipment by L&T. The aforesaid services were provided in countries outside of India viz. Vietnam and China etc. and were in relation to overseas EPC projects undertaken by L&T. Before the Assessing Officer the assessee contended that the aforesaid receipts are not taxable in India because of exclusion clause under Section 9(1)(vii)(b) of the Act. The assessee's contention was that the services were provided by the assessee outside of India and hence the aforesaid receipts are not taxable in India. However, the Assessing Officer did not agree with the contention of the assessee for the reason that manufacturing of gas fire equipment has been done in India by L&T and the manufactured equipment has been supplied to the non-resident third party. The Assessing Officer further held that mere location of the person placing an order being outside India does not shift the source of income and economic activity outside India. The Assessing Officer held that the economic activity of manufacturing to which the technical services pertained were carried out entirely in India. In appeal, DRP did not agree with the contention of the assessee and held that the assessee is not carrying out any business outside India and the business is being carried out from India, for which the FTS has been paid.

24. In appeal before us, the Counsel for the assessee submitted that the payment for services was received in bank accounts outside India. The services were rendered outside to L&T for its overseas customers. The services are connected with the EPC Contract of L&T for erection and commissioning of coal gasification plant outside India namely in China and Vietnam. The Counsel for the assessee relied on the decision rendered by the Jurisdictional High Court in the case of Motif India Infotech Pvt. Ltd. in ITA No. 1177 of 2018 wherein the Gujarat High Court held that the source of income is outside India since assessee's customer work based outside India. Further, the Counsel for the assessee also placed reliance on the decision of Bangalore ITAT in the case of Titan Industries Ltd. 11 SOT 206 wherein it was held that when the customers of the company are located outside India, then the source is outside India.

25. In response, Ld. D.R. placed reliance on the observations made by the DRP and AO.

26. We have heard the rival contentions and perused the material on record. On going through the facts of the instant case, we observe that the assessee entered into contract for provision of engineering services related to coal gasification equipment to be installed at the plant site in Vietnam and China. We observe that the services were to be rendered primarily from the office of the assessee located at Germany. Further, from the terms of the services it is seen that the services on relation to installation of equipment at China. Further, it has been also submitted before us that payment for the aforesaid services were received outside of India. It would be useful to reproduce the relevant extracts of the ruling rendered by the Gujarat High Court in the case of Motif India Infotech Pvt. Ltd. (supra) which held that as per clause (b) of Section 9(1)(vii) the income by way of fees for technical services payable by a person who is a resident of India would be deemed to accrue or arise in India. However, this clause contains two exceptions namely where the fees are payable in respect of services utilized in a business or profession carried on by such person outside India, or it is for the purpose of making or earning any income from any source outside India. In other words, therefore, if the assessment of an assessee falls in either of these two clauses, the income by way of fees or technical services paid by the assessee would still not be covered within the deeming clause of Section 9(1)(vii) of the Act.

27. In the present case, the Commissioner (Appeals) and the Tribunal have accepted assessee's factual assertion that the payments were for technical services provided by a non-resident, for providing services to be utilized for serving the assessee's foreign clients. Thus, the fees for technical services was paid by the assessee for the purpose of making or earning any income from any source outside India. Clearly, the source of income namely the assessee's customers were the foreign based clients of L&T and the services were also to be performed in locations outside of India. In this case, from the facts placed on record in our view, L&T has made payment for utilization of the services provided by the assessee in business carried out by L&T outside of India. The services which were provided by the assessee were utilized by L&T in respect of its plant set up in Vietnam and China for its foreign clients. respectfully following the decision of Motif India Infotech Pvt. Ltd. (supra), this ground of the assessee's appeal is allowed.

28. In the result, assessee's appeal with respect to the aforesaid ground is allowed.”

The ld. DR fairly agreed to the same.

54. In view of the above, the issue admittedly is covered in favour of the assessee by the decision of the ITAT for Asst. Year 2011-12, and the relevant finding of the ITAT reproduced above, the addition made by the Revenue on account of income received from L&T services, as fee for technical services under section 9(1)(vii) of the Act, amounting to Rs.73,92,399/- is deleted.

Ground no.5 is allowed.

55. Ground No.6 reads as under:

“6. Short credit of Tax Deducted at Source ('IDS') - INR 10,69,502 The learned AO has erred on the facts and in circumstances of the case and in law in giving short credit of TDS to the extent of INR 10,69,502.”

56. The issue is related to short credit of TDS given to the assessee to the tune of Rs.10,69,502/-.

57. The ld. counsel for the assessee contended that necessary rectification order in this regard has already been passed by the AO, and therefore, this ground has now become infructuous.

In view of this submission of the ld. counsel for the assessee ground no.6 is dismissed as infructous.

58. In the result, the appeal of the assessee is partly allowed for statistical purpose.

59. Now we take up the assessee’s appeal for Asst.Year 2015-16 in ITA No.1783/Ahd/2019.

60. As stated in paragraph 2 above of this order, the facts, grounds, and issues involved in both appeals for the assessment years 2014- 15 and 2015-16 are identical, except for the variation in the quantum of additions. Consequently, as fairly agreed by both the parties, the arguments and submissions made by them, as well as our observations and findings regarding the assessment year 2014-15, are equally applicable to the assessee's case for the assessment year 2015-16. Based on this premise, and after going through the grounds and issues in light of the material on record, we adjudicate the appeal for the assessment year 2015-16 by adopting the same reasoning and logical conclusion as for the preceding year. Accordingly, the appeal is partly allowed for statistical purpose.

61. Now we take up the Revenue’s CO in CO No.20/Ahd/2022.

The grounds raised in the CO read as under:

“a. On the facts and circumstances of the case and in law, whether the executed Power of Attorney notarized in The Netherlands is done in the presence of Diplomatic & Consular Officer authorized under Section 3 of the Diplomatic & Consular Officers (Oaths & Fees) Act, 1948 ;

b. On the facts and circumstances of the case and in law, whether The Netherlands falls under the list of such nations which are authorized by the Central Government in Section 14 of the Notaries Act, 1952 ;

c. On the facts and circumstances of the case and in law, whether the Power of Attorney has been stamped within 3 months after bringing it into India and if the same was done, whether done in the presence of Indian Diplomatic or Consular Officer ;

d. On the facts and circumstances of the case and in law, whether the Power of Attorney has been executed in accordance with Section 26 of The Registration Act, 1908.

e. On the facts and circumstances of the case and in law, whether the Power of Attorney has been executed in accordance with The Power of Attorney Act, 1882.

f. On the facts and circumstances of the case and in law, whether the Power of Attorney is covered by the Hague Convention of 5 October, 1961 (Apostille Convention)

g. On the facts and circumstances of the case and in law, whether the Power of Attorney falls within the definition of a Public document as defined in Section 74 of the Indian Evidence Act, 1872, in order to avail the benefit of the Hague Convention of 5 October, 1961 (Apostille Convention).”

62. This issue, it was stated, raised by the Department was considered by the ITAT in the Stay Petition filed by the assessee for Asst. Year 2007-08 to 2010-11 and 2014-15 in SA No.11 to 14/Ahd/2022, and the ITAT rejected the contentions, noting that person signing the appeal was a valid power of attorney holder which was sufficient for filing of a valid appeal.

The ld. DR fairly agreed with the same.

63. In view of the above submissions of both the sides, the cross objection filed by the Revenue is dismissed.

64. In the result, the appeal of the assessee is partly allowed, while the CO filed by the Revenue is dismissed.

Order pronounced in the Court on 18th December, 2024 at Ahmedabad.

DISCLAIMER: Though all efforts have been made to reproduce the order accurately and correctly however the access, usage and circulation is subject to the condition that publisher is not responsible/liable for any loss or damage caused to anyone due to any mistake/error/omissions.